Following on from my previous post, I wanted to sketch out what making electricity cheap in the UK could really look like. I then rapidly discovered that trying to cover everything I wanted to say on this topic in a single post would almost certainly abuse the attention span of my readers. This post is going to cover what I believe the most systemic issue facing power prices is - market power - and how we tackle it. The next post(s) will cover the discreet interventions I would recommend as I play Fantasy Britain Mega-Engineer.

Managing legacies

I think of the electricity market as being rather like Rome, that eternal city. Each set of reforms is built upon a layer of existing market structures. Occasionally reforms will dig a little deeper and change the underlying structures of the market, but typically speaking our decadal bouts of reform tend not to touch the structures that lie beneath. From the New Electricity Trading Arrangements in the 2000s to Electricity Market Reform in the 2010s and to the Review of Electricity Market Arrangements that is ongoing, one could still pluck a trader from 2004 through time, put them at a Bloomberg terminal and they’d still have a reasonable idea of what is going on. Once you’d explained to them what a TikTok is, of course.

The problem is that you now have a great deal of what you might want to call technical debt that has accrued over the last thirty to forty years. Processes designed for analogue systems, structures designed around the interests of large incumbents, and rules that facilitate a system based on coal power stations built near coal fields.

One of the key criticisms that’s been made of these legacy structures is of the wholesale market. We have a single national price that reflects the scarcity of power in half hour slots. This price is set by the most expensive plant that it’s necessary to turn on in that window, invariably gas. This means that plants with effectively zero marginal costs of production, like wind or solar, get paid the same as that pricey gas plant. And this has led a range of commentators to call for the decoupling of such prices from the headline wholesale price.

But to call for this is to misunderstand how power trading actually works, because the price is not set by gas, it’s set by trading. The wholesale market is a short-run market; it sets prices close to real time. If you establish a long-run market - say, through mandating that all green power producers sell their power into a pool at a fixed price which is then sold on to industry at that price - then the eventual consumer of that power is entirely able to sell that power on the short-run market. The only way you can avoid such markets interacting is through a mechanism like the Contract for Difference which essentially obliges generators to only recover revenues in line with a fixed price, even if their sell price is different.

In my last post, I said that the gas price was the reason industrial power prices are going up. But if trading sets the price of electricity rather than the gas price, doesn’t that contradict that claim?

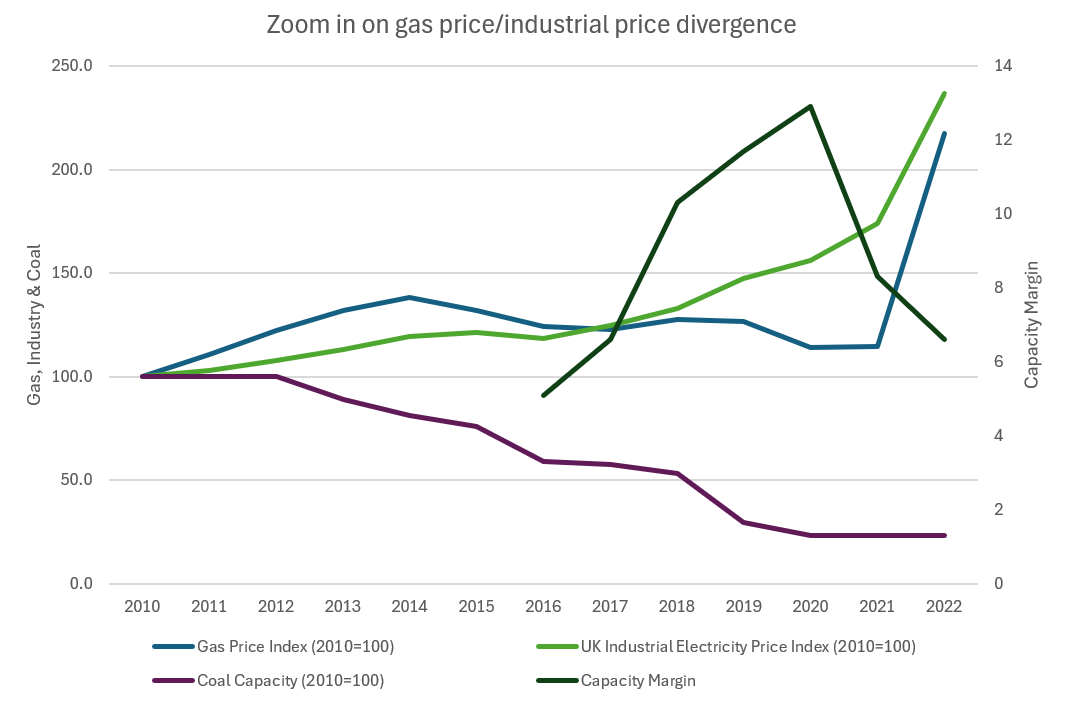

Unfortunately not. The chart in my previous post showed a clear correlation between the gas price and the industrial electricity price that only diverges in about 2017-18. Let’s dive into what’s happening in that period:

The post-2017 divergence is primarily driven by coal coming off the system, as well as an effect of tighter capacity from 2020 onwards. In the period above 18GW of coal shut down. And this is where trading comes in again.

Dark and Sparky Spreads

Electricity traders spend a lot of time thinking about the ‘dark spread’ and the ‘spark spread’. The ‘dark spread’ is the difference between the price of power produced from coal and the actual price of power, and the ‘spark spread’ is the difference between the price of power produced from gas and the same. During much of the 2000s when coal was relatively cheap, if the dark spread widened the spark spread would turn positive as gas plants came into the money, and vice versa when gas was cheap. This effectively put a ceiling on how expensive power from either source could go. But if traders no longer need to be concerned with the dark spread because all the coal plants are closed, then the spark spread becomes the difference between the price of gas and the highest price they can charge for power before people start switching it off. And demand for power is rather inelastic.

The absence of coal - even with relatively healthy capacity margins - handed considerable market power to gas-fired power plants, and although gas still sets the price of power, it does so at a heftier margin than in the 2010s. One can observe this by looking at the gross profits of Uniper UK, whose primary business is running gas power plants:

You’ll note that this tracks the shape of the industrial electricity prices curve rather better than it does the shape of the gas price curve.

It is this effect - the market power that a particular technology group or set of assets has - that I believe is fundamental to driving down the cost of power. But it is an effect that is wholly under-served in existing policy, and there is a clue as to why in the zoomed in chart above. The capacity margin, which is in effect a measure of system resilience, seems to have very little to do with power prices. The significantly higher margin in 2018-2020 should have had an impact on market power. And yet, it didn’t.

A Brief History of Capacity

To understand why, we need to delve into the history of this measure. It is essentially a measure of whether there is adequate generation on the system to ensure system security in the event of a demand spike. Historically Loss Of Load Expectation (LOLE) has also been used, but the capacity measure acquired a particular importance in its role in establishing the Capacity Market.

The Capacity Market is a measure introduced as part of the Electricity Market Reform process in the 2010s that was intended to buy a new generation of CCGTs, which it spectacularly failed to do. The reasons are manifold, including renewables cutting into the running time of gas assets, but the primary reason is that the Capacity Market was intended to provide system security rather than improve day-to-day market liquidity. This meant it primarily bought assets that had an excellent capex-to-capacity ratio, which turned out to be gas turbines installed in shipping containers in car parks throughout the country.

We had bought a secure system, but let’s not pretend 80 tiny car park gas turbines had any kind of market power. They were inefficient to run and therefore had the equivalent of a very wide spark spread, leaving pricing power with the legacy CCGT fleet. This effect was concealed while coal was in the system, but is now fully exposed.

We are now about to shut down even this CCGT fleet in order to achieve Clean Power by 2030, and it is here that my biggest worry lies. I fear we are about to repeat the same mistake as we did with the original Capacity Market.

Good Chaps Discharge Last

NESO’s Clean Power 2030 generation mix has been designed to ensure that a 2030 system can operate securely. But it suffers from the same issue that underlies most system-level models: the assumption that everyone will be good chaps, accept a given return and not seek to rinse the consumer for all they can.

Under both the scenarios the volume of assets that could conceivably have market power is very low, which means higher prices. To understand this, you need to not think like a system designer, but like a trader, and look at the information market participants will have available to them.

Renewables are not subject to price effects, only volume risk, but will deliver abundance on the days when the weather complies. The price will still be set the rest of the time by a limited number of technologies: batteries, longer duration storage, interconnection and perhaps a very small volume of gas with CCS.

Power consumption data is publicly available via the Balancing Mechanism Reporting Service. This means that if you know the capacity of a battery or a bigger store, you also know its level of charge. Everyone competing in this space will have perfect visibility of their competitors’ charge state and therefore can seek to optimise their own discharge over the course of the day. What ‘optimise’ means in this context is charge as much as you can get away with.

Your ability to ‘optimise’ is dependent on your ability to capitalise on opportunities throughout the day, and therefore is a function of the size of your energy store. This means that bigger stores will have significant market power. They will effectively be CCGTs for the purposes of the post 2030 market. And herein lies my biggest criticism of the CP2030 work.

NESO sees a range of bigger store capacity in 2030 of between 4.6-7.9GW, the bulk of which will be pumped hydro in Scotland and therefore behind a grid constraint and potentially irrelevant for price-setting a lot of the time. The 2030 system risks not simply having pricey peaks during low renewable output times, but pricey days when renewable output is at a middling ebb and a very small number of stores are setting the price in the entirety of England. The only saving grace might be interconnection acting as a price ceiling, but delivery of these assets to France at least is proceeding at a snail’s pace as post-Brexit issues endure.

Captured Abundance

What this means for 2030 is that we should seek to permit and connect as many big stores as possible, especially the locationally fungible technologies like compressed or liquid air. The Government is currently in the process of, once again, refusing to learn the lesson of the success of the CFD auction in lowering costs and has instead commissioned Ofgem to carefully evaluate all the big storage projects for a cap and floor support scheme and pick its faves for support.

A cap and floor means that these assets will have a guaranteed return - the ‘floor’ - and pay back any revenues above a certain level - the ‘cap’. This helps at least ensure they don’t exert too much market power. But if we must offer support for assets that are likely to do very well, we should at least run a competition for the delta between the cap and the floor so that we can ensure we are buying the cheapest ones. Pumped hydro - the technology of much of the projects coming to market - has been around for decades, after all.

“Build more of a specific thing” therefore becomes my primary recommendation. However, I think - on the run up to 2030 - it is worth Government turning its head to look at some of the basic functioning of the market and thinking through how they could make traders permanently paranoid and afraid of trying to gouge. I do question whether we need to give all participants perfect information on what their competitors are doing for free, for example, useful as that data is for us policy wonks.

But the Government already has a rather full plate, and I would be content with them simply accepting they need to start analysing market power if they are to reduce costs on the short haul to Clean Power. In the next post, I will look at a clear concentration of market power: the monopoly networks…

Thanks Adam - learnt a lot from this! Are there any books or documents you would recommend for someone looking to learn more about the electricity market structure in the UK - and the various reforms the system has gone through?

Are you saying that battery storage in the south of England are gradually going to gain pricing power?